Guided by DSL.

The course would mainly include 2 concepts, which are Monopoly and Oligopoly.

The textbook we use is: Industrial Organization: Theory and Practice (International Student Edition) 5th Edition by Don E. Waldman and Elizabeth J. Jensen.

Lecture 1 Introduction

Fundamental Question of economics is that it is crucial to understand how production and exchange are organized.

How are products allocated to the people?

A: (mostly) through the market

Perfect market is the desire market structure

How do IO Economics Answer Questions?

Using a combination of

Micro Theory, especially Game Theory

Perfect Competition and Monopoly

Firm Behavior

Profits

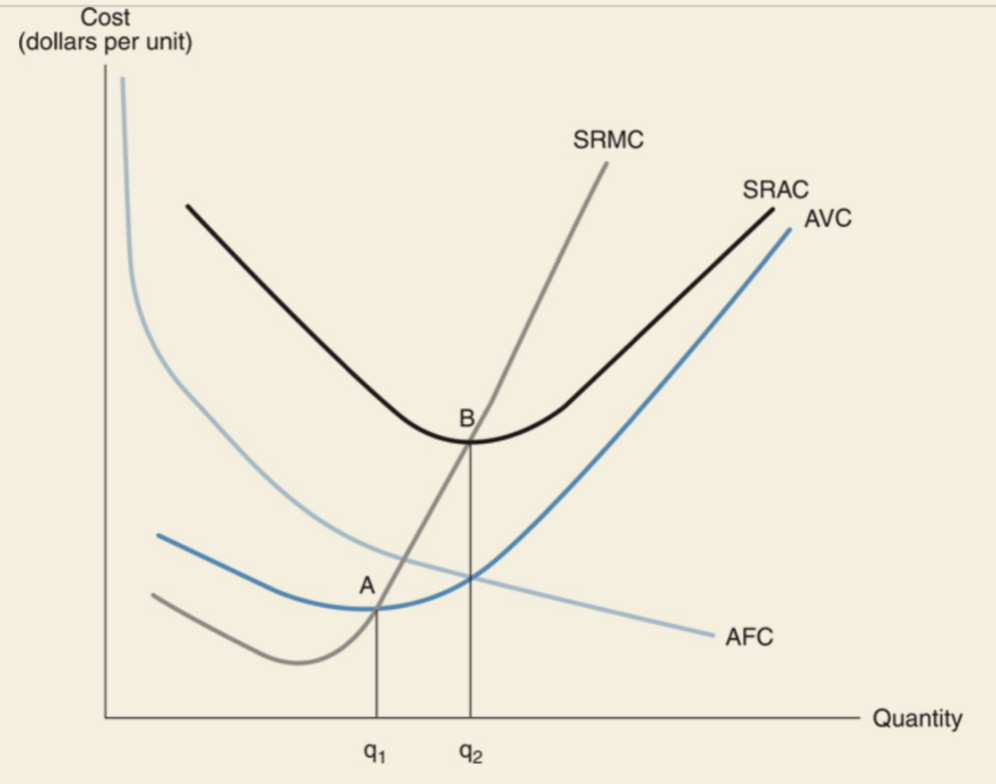

TVC stands for total variable costs. They vary with the level of output, like labor and material inputs, capital depreciation, etc.

Our definition of costs should be based on economically-based Opportunity Cost, not accounting costs.

Specifically, in a cost function, if we face an equation like:

, it is easy to justify that is the fixed cost, while the variable costs, is . (Since it depends on the quantity.)

We will sometimes refer to two concepts: